The light at the end of the tunnel

OPTIMIZATION OF RETAIL CHAINS

The crisis had a huge impact on the Russian retail market, with a significant impact on fashion retail. The retailers' response was business optimization, one of the directions of which was the restructuring of retail chains, manifested in the closure of unprofitable stores and the emergence of new ones, changing formats and rebranding. According to Inga Mikaelyan, everything that happens in online retail is a process of purification, thanks to which inefficient outlets stop working and weak players leave the market.

According to RBC Market Research, since 2015, the number of chain retailers' stores has been declining, falling from 18,652 in February 2015 to 17,160 in February 2017. About 30 international chains ceased their activities in Russia in 2015, and from February 2016 to February 2017, another 14 retailers. On the other hand, the reverse process is also observed. So, from February 2016 to February 2017, 14 international brands entered the Russian market, including Armany Exchange, Veta, Aigle, Barbour.

Over the past few years, Detsky Mir, INCITY and Familia have achieved particular success in the development of retail, opening 101, 62 and 48 stores respectively from March 2014 to February 2017. A number of players have significantly reduced their networks, including Adidas and Glance, which abandoned 248 and 42 outlets during the same time period.

The trend towards the reduction of retail chains remains quite strong and growing. So, from March 2014 to February 2015, the part of retailers that optimized business in accordance with this strategy amounted to 33%; from February 2015 to February 2016, 39%; and from February 2016 to February 2017, 50%.

The opposite direction – the growth of the number of stores in the network when opening new ones – weakens. For example, from March 2014 to February 2017, the share of players engaged in the development and increase in the number of outlets decreased from 44% to 32%. It should be noted that during this period of time, the number of those retailers who managed to keep the number of network outlets unchanged fell from 23% to 18%.

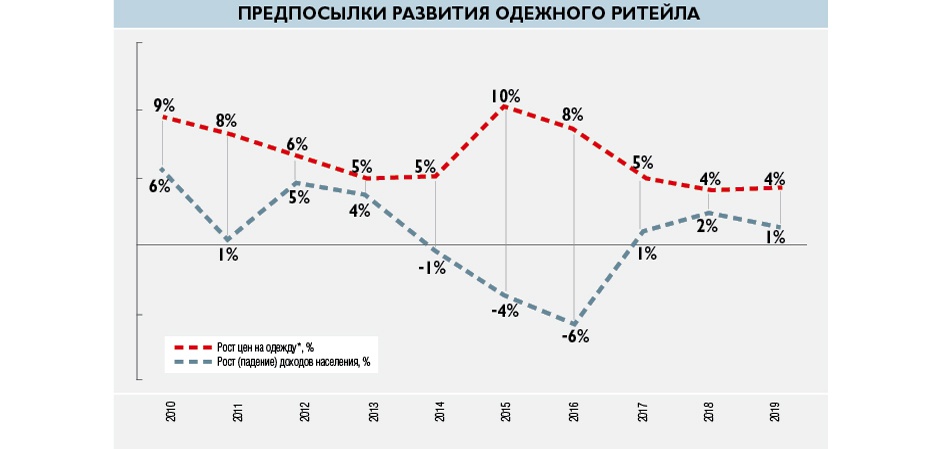

There are, however, trends with a positive meaning. Thus, despite a noticeable slowdown since 2012, the turnover of chain retailers continues to grow against the background of a general decline in the volume of the clothing market. For example, in 2016, the revenue growth of O'STIN was 13.4%; Gloria Jeans – 39.9%; ZARA, Bershka, Massimo Dutti, etc. –13.1%; H&M– 37.3%, «Children's World»– 36.2%.

Thus, the developed retail, in comparison with other market participants, occupies a more advantageous position, and this indicates that it remains the driving force, playing the role of a "locomotive" running ahead of other players.

E-COMMERCE–FASHION MARKET DRIVER

Online retail is turning into a powerful driver of domestic fashion retail. 82.4 million residents of our country are Internet users with a penetration rate of more than 70% among Russians over the age of 18. Already, according to the RBC Market Research agency, 12% of Russians prefer to make purchases via the World Wide Web. Although online sales account for only 3.3% in the domestic market, this channel has been adopted by 6 retailers out of 10. Moreover, the indicators of individual players exceed the average level, reaching, for example, 15% in Finn Flare and 4.1% in the "Children's World".

Among the online stores at the top of the rating was Aliexpress, which was preferred by 64% of the surveyed online shoppers. The second place was taken by Lamoda, which was recognized by 22% of respondents, the third - ndash; Wildberries.ru with 20% positive reviews. The list was continued by "Sportmaster" (15%), Bon Prix (13%), Ebay (12%), Ozon (11%), O’STIN (11%), Adidas (7%) and a number of others. Sales of leaders, despite the crisis, are growing rapidly. Thus, Wildberries' revenue in 2016 amounted to 37.6 billion rubles, compared with 7 billion rubles in 2012, and Lamoda's revenue was 23.9 billion rubles in 2016, compared with 2.1 billion rubles in 2012.

The spread of e-commerce is facilitated by various factors - the economic crisis, the change of generations, the development of new technologies and many others, such as, for example, the ease and convenience of making a purchase. Offline players are also making a certain contribution, who are now actively developing online sales through their own online stores, as well as multi-brand online platforms and marketplaces. The segment is expected to grow dynamically at a rate significantly exceeding the growth of traditional retail.

The development of the fashion retail market – both qualitative and quantitative – continues. This is facilitated by the rapid growth of e-commerce, the improvement of service and retail formats, including an integrated omnichannel approach, as well as the optimization of business processes, product management and the introduction of new technologies.

Among the positive changes in the consumer market are the growth of positive expectations, the desire to maintain the level of spending and quality of life, and the activation of customer behavior. The revival of the market will be accompanied by the restructuring of retail trade and the introduction of innovative directions. In the conditions of a protracted crisis and uncertainty, modern methods and flexible pricing policy will help retailers maintain their positions and attractiveness for different generations of Russians.

Text: Elena Varnina

Photo: shutterstock.com